When Direction Isn't in the Prices

What a quant model's low-conviction state tells founders about capital formation

There's a state my trading model enters maybe a few times a year where it stops being useful in an interesting way. The signal isn't broken. It's reading the market correctly. The directional information just isn't in the prices anymore.

Most market commentary lives at one of two levels: macro (rates, inflation, the Fed) or micro (this stock beat, that stock missed). The level in between, where the action actually happens, is the regime. In the standard usage, a regime is a period of stable market behavior defined across several dimensions: trend, volatility, liquidity, risk appetite. The dimension that matters most for capital formation, and the one this piece is about, is directional consensus. The state where it's missing maps almost one-to-one onto what founders and VCs experience as a freeze.

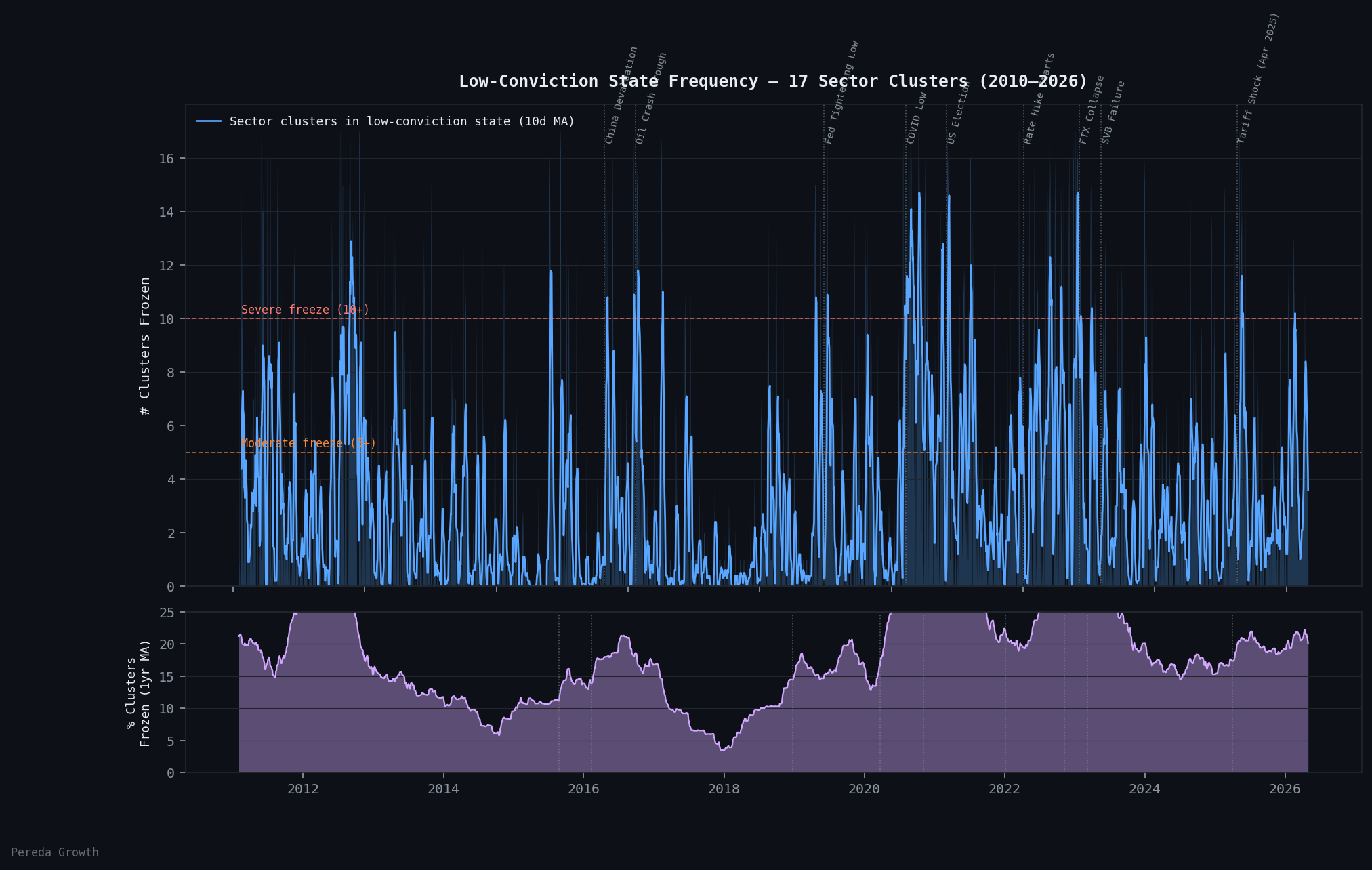

The framework here is built on sixteen years of regime detection across seventeen public equity sector clusters. Out of all that data, ninety-six distinct low-conviction episodes show up. These are periods where a cluster cannot sustain a directional edge for ten or more consecutive trading days. The single most striking moment in the dataset is one day: April 14, 2025. On that day, in the immediate aftermath of the Liberation Day tariff announcements, all seventeen clusters were simultaneously ambiguous. Every sector, no exceptions. The market collectively could not price what the rules were going to be.

What a low-conviction state actually means

Bear markets don't freeze capital. Ambiguity freezes capital. A sector can trade at compressed multiples with high conviction, where the market agrees the sector faces real headwinds, and capital still forms, just at lower prices. What stops capital cold is a sector that participants cannot agree on a direction for. Low multiples plus consensus is a buying opportunity. Any multiple level plus unresolved direction is a deployment pause. The level effect and the uncertainty effect look similar in the headlines and behave completely differently underneath.

The behavior shows up in markets as a well-documented signature. Borland (2009) 1 showed that during panic episodes, "the co-movement of stock returns increases" dramatically. Names that should be diverging start moving together. FTSE Russell observed exactly this during the 2020 COVID shock, with cross-sectional industry return correlations climbing to nearly 0.9, "virtually obliterating diversification benefits" 2. When everything moves together, every model that depends on names diverging stops working, and so does every valuation framework that depends on names being distinguishable from each other.

The largest coordinated freezes in the dataset

When I look at the sixteen-year catalog, the question that emerges is: what kinds of events produce the broadest simultaneous freezes? The answer inverts a common assumption.

The largest coordinated capital formation freeze in modern markets was not the COVID crash. It was the 2020 US election. Across the seventeen sector clusters my model tracks, eleven of them entered low-conviction states simultaneously in October and November of 2020, against eight during the COVID crash earlier that year. COVID was deeper and faster, but the election was wider and more sustained. The single-day record belongs to April 14, 2025, when all seventeen clusters were in ambiguity at once during the immediate tariff shock. But the sustained coordinated freeze, the kind that holds the market in place for weeks, belongs to the election.

Source: Analysis of 17 sector clusters, 2010–2026. Pereda Growth internal data.

The pattern across the dataset is consistent. Financial crises produce sharp, narrow freezes that resolve quickly because the new price is the new price. Once the credit event is priced, direction reasserts. Policy uncertainty produces broader, longer freezes because participants are not waiting for a price, they are waiting for rules, and rules take longer to legibly emerge. The 2020 Fed tightening cycle (4 clusters), the FTX collapse (6 clusters), and the April 2025 tariff shock in its sustained phase (3 clusters) were each more contained than either of the 2020 events. When the uncertainty is sector-specific or monetary, fewer clusters freeze. When the uncertainty is regime-level, in the literal sense of what the rules of the game will be, nearly everything freezes at once.

Two case studies in how shocks resolve

The April 14, 2025 tariff peak is worth contrasting with the 2020 election because the two look similar from the outside (both policy events, both produced multi-cluster freezes) and behave very differently underneath.

The tariff shock was a directional event in disguise. The simultaneous all-cluster ambiguity peaked at all seventeen clusters on April 14, a reading that has appeared only a handful of times in fifteen years of data, but it didn't sustain. Within weeks, most clusters had resolved cleanly into the new price level. Energy Transition was the longest holdout, with a 19-day episode through mid-May, but even that resolved with a 29 percent return during the episode itself as the market repriced energy policy exposure. By summer 2025, the dataset shows ambiguity flares dropping back to background noise levels of two to four clusters at any time. The shock was severe but the information content was high. Once participants understood what tariffs meant for which sectors, direction returned.

The 2020 election was the opposite. The shock was less severe in any given moment but the information content was low. Participants weren't waiting for a price, they were waiting for an outcome that would dictate years of policy direction. Eleven clusters held in simultaneous ambiguity for weeks. The venture deal data from that period is consistent with what the framework predicts: process starts continued, but closings collapsed. Pipelines without follow-through. Term sheets that took months to convert.

The lesson is that the kind of ambiguity matters more than the magnitude. A clear directional shock, even a violent one, resolves into a tradeable regime. An unresolved policy question, even a quiet one, can hold an entire market in deployment-pause for a quarter or more.

Why founders and VCs feel this

Every private market transaction requires two parties to agree on a valuation, and that agreement leans on three anchors (stage-dependent): public comparables, recent precedent transactions in the same sector, and discounted cash flows. None of these tools disappear in a low-conviction state. What happens is slower and more uneven, and that's actually what makes it disruptive.

Public comps go first, because they reprice every day. In the first week or two of an ambiguity window, the multiple range you'd pull from your basket of comparables starts widening. By week three, the number you would have used to anchor a term sheet at the start of the month no longer matches what the comps are saying now, and there is no obvious reason to prefer one reading over the other. The tool still produces an output. It just produces a different output every Tuesday. Commonfund notes that when financing events slow and rounds become less frequent, VC managers lean more heavily on public comparable methodologies to mark their portfolios 3, which means the instability sitting in the public market gets imported directly into private valuations.

Precedent transactions decay more slowly. A round that closed three weeks ago is still a real comp; you can defend pricing off it. A round that closed six months ago, before the regime shift, is gradually demoted from "comp" to "history." There's no single moment where a precedent stops being usable. It just gets progressively harder to argue for, and the argument requires more and more justification of why the prior environment is still relevant. By the second or third month of an unresolved regime, most precedents have crossed that line.

DCFs are the slowest to break because they're not constantly being repriced, and at early stages they barely apply at all. Seed and Series A rounds rarely turn on a DCF; the math is mostly about ownership targets and milestone runway. By growth and late stage, DCFs come back into the picture as a sanity check on multiples, and that's where the regime instability shows up. The discount rate in a DCF is partly sector beta, and beta is unstable when dispersion is high and direction is unclear, which means two reasonable analysts can build the same DCF in the same week and arrive at materially different terminal values. The tool works. It just stops producing convergent answers.

The deterioration also isn't uniform across companies. A company with strong independent signals, real revenue growth or real profitability, can shrug off most of this. The buyer doesn't need the comp to anchor because the company anchors itself. The freeze hits hardest on companies whose valuation case relies on sector tailwinds, because that's exactly where comp instability translates directly into "I can't defend this number to my partnership." The companies that get done in low-conviction regimes are the ones that don't need the regime to make their case.

Buyer and seller end up holding fundamentally different views of what the company is worth, neither can defend their position with market data the other side accepts, and transactions stop happening. This is not a multiple compressing. This is the loss of shared reality required for a multiple to mean anything.

That breakdown propagates through your business in stages. The first stage is your customers. Enterprise CFOs run on three things to approve software spend: a defensible ROI model, board confidence the vendor will exist in three years, and political cover from peer adoption. A low-conviction sector regime breaks all three. The ROI model assumes stable input pricing on both sides of the trade, which a high-dispersion environment doesn't provide. Vendor survival becomes an open question when fundraising freezes and runway compresses across the sector. And the "everyone in our space is buying this" argument disappears when there is no shared sense of where the space is going. The CFO who would have green-lit your tool last quarter is now asking for a six-month deferral, and they are not lying when they say it's about timing.

The second stage is your investors, with a longer lag. Anyone who has sat in a partnership meeting knows that VC valuation is partly a social process, not just a financial one. The lead investor proposes a number, the other investors stress-test it against their own comp tables, the partnership debates it, and the founder accepts or pushes back based on what other firms are saying. All of those steps depend on shared anchors. When the underlying comps are unresolved, every step in that chain slows down. Term sheets that used to take ten days take three weeks. The gap between what a lead is willing to propose and what a founder is willing to accept widens, sometimes to the point where the round just doesn't get priced.

That last problem is where deal structure starts to bend. When nobody wants to set a number they'll have to defend later, bridge rounds and SAFEs replace priced rounds. Existing investors extend runway with a convertible at the prior cap, or with a discount to the next round, specifically because committing to a fresh valuation in the current regime feels indefensible. From the founder's seat this looks like investors hedging. From the inside it's the rational response to comps you can't anchor to. The structural signature of a low-conviction regime in venture isn't fewer dollars deployed. It's the same dollars deployed in less committal structures.

The reason all of this lags the public market is partly social and partly mechanical. JPMorgan's Ginger Chambless has noted "a one- to two-quarter lag between public market corrections and corrections in private markets" 4, and Thomvest's Don Butler has put the historical lag from the 2008-09 cycle at six to nine months 5. The mechanism is straightforward: private markets don't have a daily mark-to-market exchange, so the public signal has to leak through indirectly. Through customer behavior. Through analyst notes. Through the eventual closing of comparable rounds. None of those channels are fast.

If you are pitching into a regime like this and finding it harder than it should be, the problem is probably not your deck.

The harder case: when the regime never comes back

Most ambiguity windows resolve. The market reads the new rules, prices them in, and direction returns. But sometimes the regime change is permanent, and that's the version founders need to be ready for.

Pre-2020, I had a signal trading earnings reversals. Stocks that moved sharply on earnings would systematically revert in the following days. After 2020, in my own out-of-sample testing, it broke. The magnitude of post-earnings moves actually increased. Stocks were moving more, not less, in response to earnings prints. But the directional predictability collapsed.

What I think I'm seeing is part of a longer structural shift in how earnings information gets absorbed. Milian (2015) showed that for firms with actively traded options, the historical post-earnings drift pattern can actually flip sign: easy-to-arbitrage firms in the highest decile of prior earnings surprise underperform the lowest decile by 1.59 percent at their next announcement 6. A 2023 cross-country study of 41 markets found that algorithmic trading is associated with a measurable decline in post-earnings drift, concluding that "algorithmic activity appears to encourage a rapid absorption of earnings signal close to financial disclosures" 7. The literature isn't pointing at exactly the signal I traded, but it is pointing at the same underlying mechanism: when options markets and algorithmic positioning absorb the post-announcement imbalance, the patterns that human-paced repositioning used to produce stop showing up. My signal was one of those patterns. It worked when institutions had to physically reposition after a surprise. It stopped working when the repositioning was already done by close on announcement day.

The line between this and what founders face is more direct than it looks. Some shocks pass. Customers come back, valuations re-anchor, narratives reform. Other shocks change the structure of the market permanently, and the assumptions your company was built on stop being true. The hard problem is that during the shock itself, the two cases look identical. Both produce stalled pipelines, deferred decisions, and unsigned rounds. You cannot tell from inside the disruption whether you are waiting out a transient regime or watching your foundational thesis quietly invalidate.

The way I try to tell the difference is to ask three questions. First: has the channel by which value flows changed, or just the price at which it flows? Tariff shocks change prices; supply chains and customer relationships still work the same way once the new prices settle. A new regulatory regime, by contrast, can shut down a channel entirely. Second: are the buyers who were active before still in the market, even at lower volume? If the same accounts are still buying and the cycles are just longer, the mechanism is stressed. If a class of buyer has structurally exited (new compliance burden, new procurement model, new internal alternative), the mechanism is broken. Third: is the substitute that pulled customers away getting better over time, or is it a one-time reallocation that can reverse? Substrate shifts, like new technology that does the job ten times cheaper, don't reverse. They keep compounding. Cyclical pullbacks do reverse.

Tariff shocks stress mechanisms. They don't usually disrupt them. New regulatory regimes, new dominant participants in a market, and new technological substrates disrupt mechanisms, and the old regime doesn't return. If you are building in a space where the underlying market structure has shifted, no amount of patience saves you. You have to rebuild the company's relationship with the new world.

What's happening right now

As I write this, the broad market has just completed a resolution out of an ambiguity window. February through April 2026 saw a second cluster freeze, with several sectors entering low-conviction states. Over the past two weeks, that ambiguity has cleared. Most clusters are now showing decisively bearish directional readings: not panicked, not crashing, just leaning down with conviction. Importantly, the absolute price level is still elevated; clusters in aggregate are trading roughly 22 percent above their January 2025 baseline. The "bearish conviction" is a modest pullback from a peak, not a collapse. What that means in practice: capital can flow again. Bear regimes are tradeable. Founders and VCs operating in most sectors right now should be experiencing something different from the freeze of the last quarter, even if the headlines feel worse.

The exception, and it's a meaningful one, is AI & Cloud Infrastructure. As of last week's data, AI/Cloud is the only cluster still in a low-conviction state, sitting right on the threshold. It might extend, it might resolve in the next few sessions. Either outcome is interesting, but the structural observation is more important than the daily reading: AI/Cloud has historically been one of the most freeze-prone clusters in the entire dataset, and consistently among the last to resolve when ambiguity windows clear.

The reason isn't sentiment in some vague sense. It's that AI/Cloud is structurally one of the hardest clusters in the market to price. The basket holds at least three competing narratives at once: pure compute infrastructure (chips, hyperscaler capex, training clusters) trading on one set of assumptions, application-layer software trading on a different set, and the commoditization story trading against both. Capex commitments and revenue realization are on different time horizons, often by years. The smaller names are heavily dependent on three or four hyperscalers whose own capital plans can move the entire cluster on a single earnings call. When you put all of that into a single basket, dispersion stays high almost by construction, and the market needs longer than usual to assemble a consensus view on direction. That's the regime founders building AI infrastructure or selling into hyperscaler capex are in right now. The rest of the market has decided. Their sector is still working it out. Plan accordingly.

What to do with this

I'm not going to pretend regime models are a directly portable tool for founders. They take time to build, they require data infrastructure most companies don't have, and the discipline to act on probabilistic signals is not natural for most operators. What I do think is portable is the question, and more importantly the signal.

The diagnostic for "am I currently in a low-conviction regime" is the easy half. Pick the public cluster that most directly maps to your sector. If correlation within the cluster has spiked and the names are all moving together, if implied vol is elevated and realized vol is choppy, if the spread between the best and worst performers in the basket has compressed, you are in it. The things you are experiencing in your pipeline are explainable by that. Plan accordingly. Conserve runway. Resist the pressure to drop pricing to close stalled deals, because the deals are stalled for reasons that have nothing to do with your pricing.

The harder and more useful half is reading the resolution. The actionable moment is not when you're in the regime. It's when you're coming out of it. And here the data has a specific shape that most founders and investors get wrong.

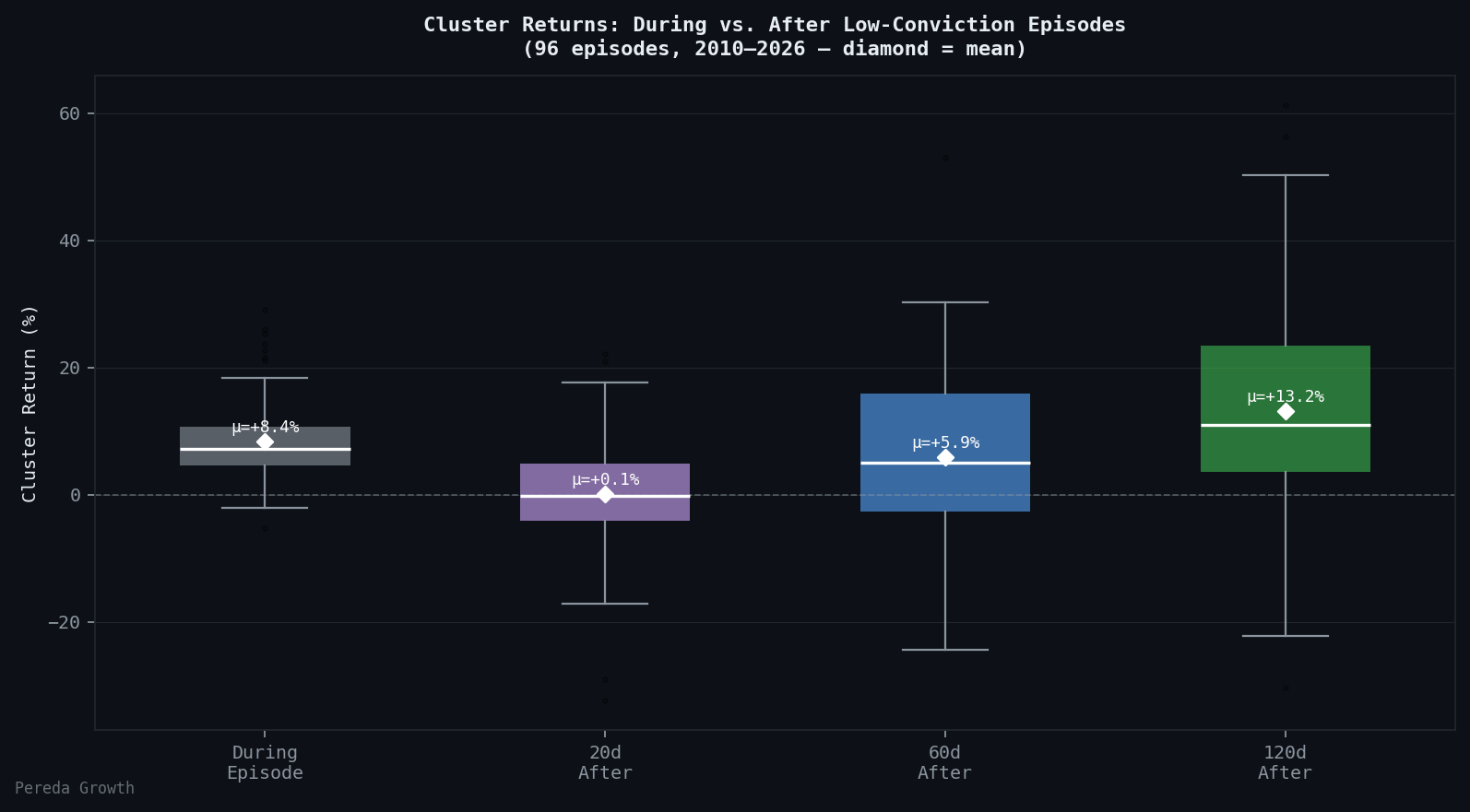

Looking across sixteen years of regime data and ninety-six distinct low-conviction episodes, the result worth knowing is that resolution does not mean recovery. In the twenty trading days following an episode end, average cluster returns are essentially flat, near zero. By sixty trading days, the average runs roughly six percent. By one hundred and twenty days, thirteen percent. The signal resolves cleanly, and then the market spends the better part of a month rebuilding conviction before returns diverge meaningfully from zero.

Source: Analysis of 96 low-conviction episodes across 17 sector clusters, 2010–2026. Pereda Growth internal data.

The mechanism is a downstream cascade. The public price signal resolves first. Sell-side analysts update price targets in the first week or two. Earnings revisions follow. Buy-side recommendations shift. Enterprise buyers and venture investors, who are further down the chain, only begin acting on the new regime four to eight weeks after the public market has technically called it. The near-zero twenty-day return is not weakness in the resolution signal. It is the gap between when the signal fires and when the deployment opportunity becomes obvious to everyone.

For founders, that means the right time to start a fundraising process is not when your sector resolves. It is roughly four to six weeks after, when the public evidence has had time to accumulate but before the consensus has fully reformed. Three observable signs that resolution has actually happened: your sector's public basket has been trending in one clear direction for three or more consecutive weeks, the top three to five public comps for your business are all moving the same way rather than walking around, and recent comparable private rounds have actually closed, not just been announced or led with no follow-through. When all three line up, the window is opening.

For investors, the same finding cuts the other way. By the time resolution is obvious in the private deal data, you are late. The model resolves first, the public market resolves next, and the private market is the last leg of the cascade. The right response to a low-conviction state is not to sit out. It is to maintain portfolio support so existing companies don't run out of runway, build conviction on individual names independent of the sector signal, and pre-position term sheets four to six weeks before you expect public resolution to translate into private market action. The asymmetric recovery curve is the empirical case for being early.

Most of the market is past its ambiguity window now. AI and Cloud is still working its way through. Founders and VCs in that corner of the market should expect their freeze to lift later than the rest. That's the structural pattern across sixteen years of data, and it's the regime they're in today.

Public markets resolve in days. Private markets resolve in quarters. The whole game is in the lag between them.

References

All empirical findings on cluster regime states, episode counts, and post-resolution returns are based on analysis of internal data covering 17 thematic equity clusters from January 2010 through May 2026. Episode definitions and methodology are proprietary to Pereda Growth.

Footnotes

-

Borland, L. (2009). "Statistical Signatures in Times of Panic: Markets as a Self-Organizing System." arXiv:0908.0111. https://arxiv.org/pdf/0908.0111 ↩

-

FTSE Russell (2022). "Dispersion throws investors a lifeline in volatile pandemic era." https://www.lseg.com/en/insights/ftse-russell/dispersion-throws-investors-lifeline-volatile-pandemic-era ↩

-

Commonfund (2025). "Venture Capital Valuation 'Marks': What's in Your Wallet?" https://www.commonfund.org/cf-private-equity/venture-capital-valuation-marks-whats-in-your-wallet ↩

-

Chambless, G., as cited in CAIS (2022). "Public Market Weakness and Venture Valuations." https://www.caisgroup.com/articles/public-market-weakness-and-venture-valuations ↩

-

Butler, D. of Thomvest Ventures, as quoted in Crunchbase News (2022). "Are The Good Times Over? Startup Valuations Dip." https://news.crunchbase.com/venture/startup-vc-fundraising-valuations-falling-2022/ ↩

-

Milian, J.A. (2015). "Unsophisticated Arbitrageurs and Market Efficiency: Overreacting to a History of Underreaction?" Journal of Accounting Research, 53(1): 175-220. ↩

-

"Algorithmic Trading and Post-Earnings-Announcement Drift: A Cross-Country Study" (2023). International Journal of Accounting. https://www.worldscientific.com/doi/10.1142/S1094406023500038 ↩